Share this ![]()

July 3, 2024

US Men’s National Soccer Team Eliminated from Copa America

The thing that gets me about this one is the apparent lack of mental preparation for the Panama game. Everyone knew Uruguay was going to be a tough match. But with Panama, it felt like an easy win – an opportunity to widen our goal differential and improve our odds of advancing to the knock-out stage. We lost to Panama and then to Uruguay – no surprise on the latter. What happened? I’m looking at you, Gregg Berhalter! Why wasn’t winger Tim Weah prepared to deal with that level of instigation? Why was he so quick to throw hands and get a red card? I digress. The overarching lesson here is: “don’t get caught unprepared!” The same goes for hedging your interest rate exposure. Let’s touch on the general economic highpoints that have transpired over the past few months and then dive into the numbers.

Economic Overview

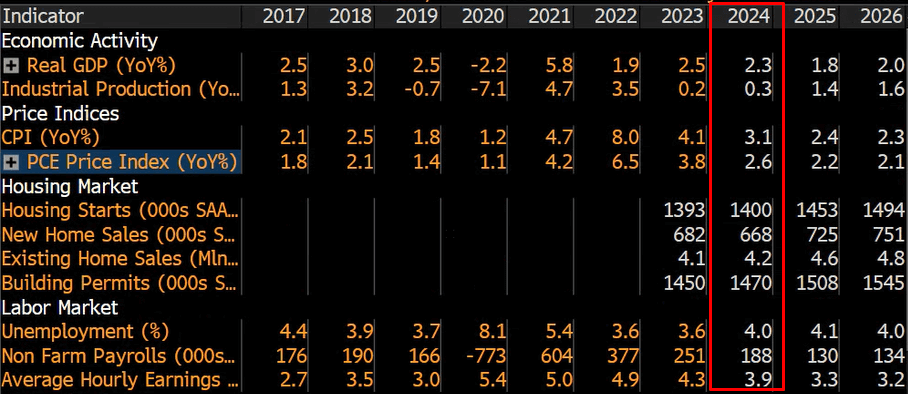

The economy continues to hum along. GDP is projected to come in slightly above 2%, with consumer price index (CPI) hovering around 3%. Unemployment projections have increased slightly to 4% but is still a far cry from the doldrums of the COVID era Equities continue to trade at or near all-time highs, though it’s worth noting that the Dow Jones index appears to have leveled off a bit over the past three months.

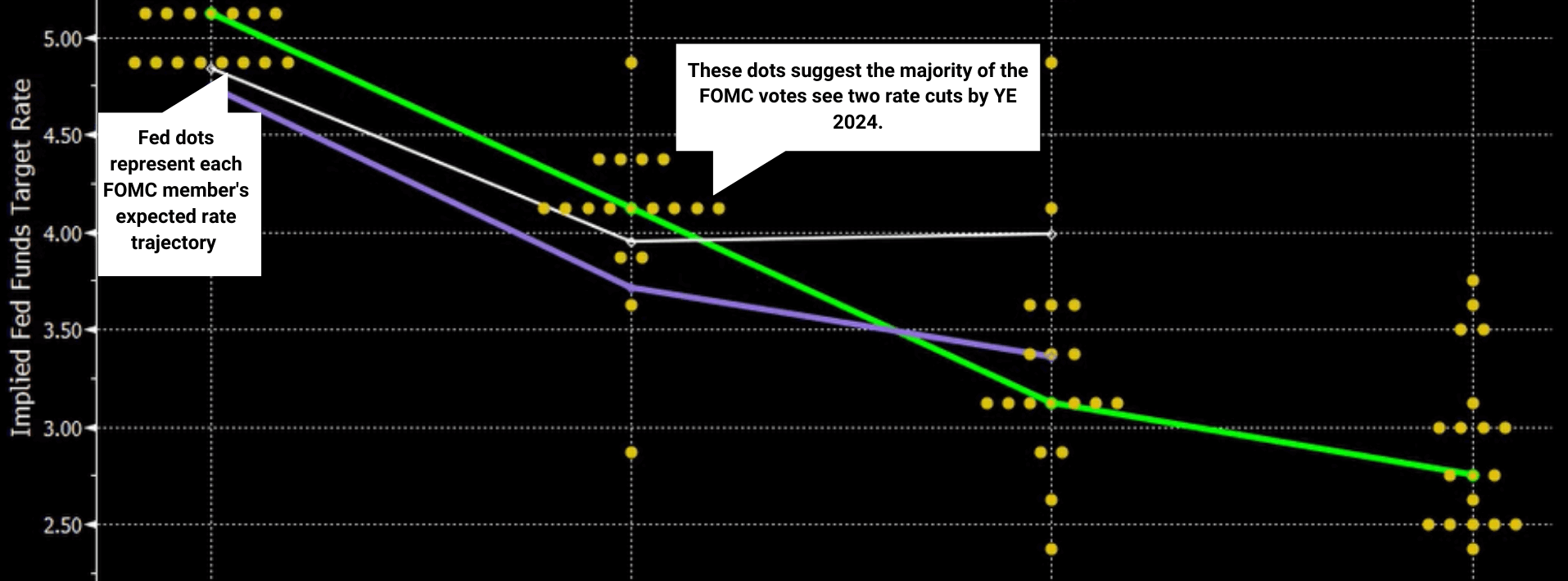

Fed Chair Jerome Powell has said the latest economic data looks promising, with inflation presumably heading in the right downward direction. He added, however, that he would still prefer to see more evidence before cutting rates. Dot plot consensus is still two cuts by year end.

Interest Rates and Borrowing Strategies

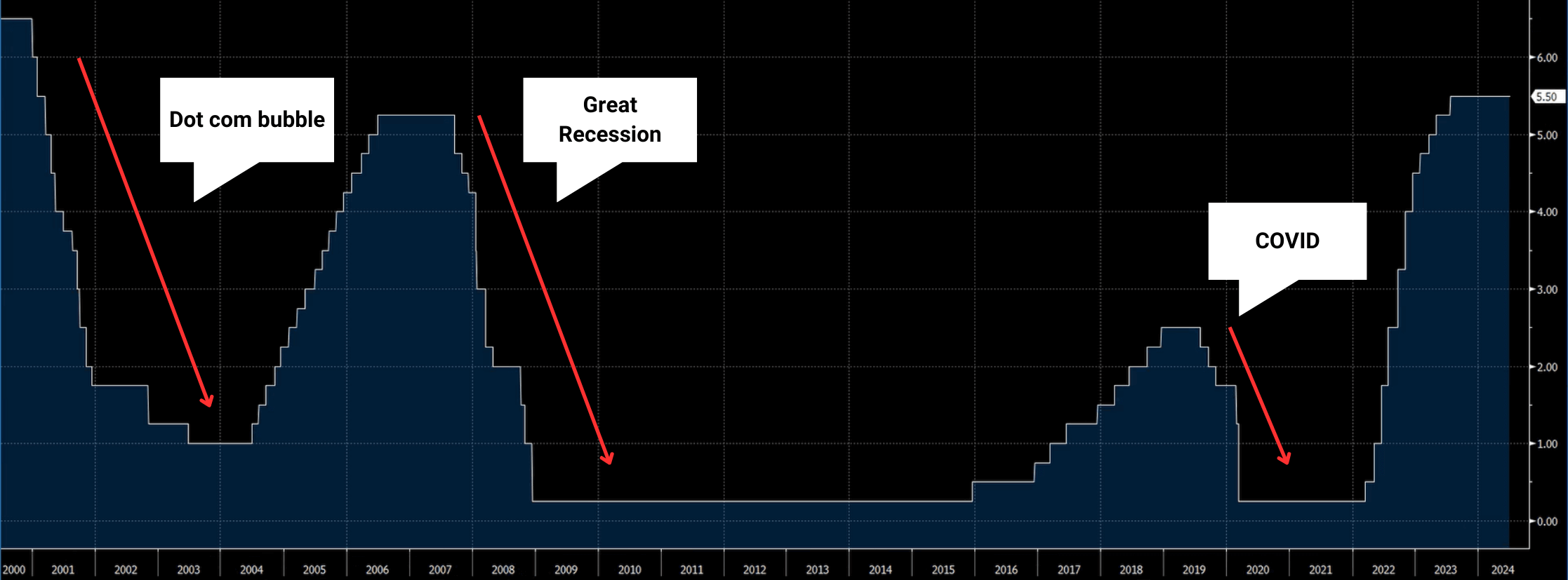

It appears interest rates will remain at elevated levels with the Fed’s continued “wait and see” approach, choosing no action until economic data points to a clearer signal that action is needed. Let’s remind everyone of the historical trend in long-term rates: as soon as the Fed starts cutting short-term rates, long-term rates fall off a cliff. The big question is “when?” The best guess, based on market data, is December of this year, after the elections, when there is more certainty on what policy will look like for the next four years.

This has led some of our borrowers to employ a shorter-term tenor strategy when it comes to hedging their interest rate exposure. This strategy allows for the elections to play out and gives some breathing room for rates to come down. In a normal market, our borrowers prefer 10-year terms to align with the term of their leases (usually 10 years or longer). This creates a nice arbitrage situation where owners/landlords can borrow against the property (underlying collateral) that is being leased at a cap rate above the interest rate. That is to say, 10-year term debt at 6.0% while you have a 10-year lease at an 8.0% cap rate would create a roughly 200 basis point spread in favor of the owner that is locked in over a long term.

With shorter tenors, this allows for an enhanced opportunity to lock in arbitrage today while also planning for an eventual rate cut, further enhancing the spread once the Fed begins to cut rates.

Conclusion

You can have your cake and eat it too. Consider taking on shorter-term tenors that are not only cheaper on the front end but also provide the flexibility to refinance in the short term. The goal here is that once rates come back down, you are well-positioned to further enhance your returns as it relates to your medical real estate investment. Don’t get frustrated with rates being higher for the short term and pull a “Weah.” Cooler heads prevail. Employ a strategy. Talk with the experts, get an outside opinion from Gregg Berhalter CMAC Partners. Cheers!

by Chris Tollinchi

Share this ![]()