Share this ![]()

July 8, 2024

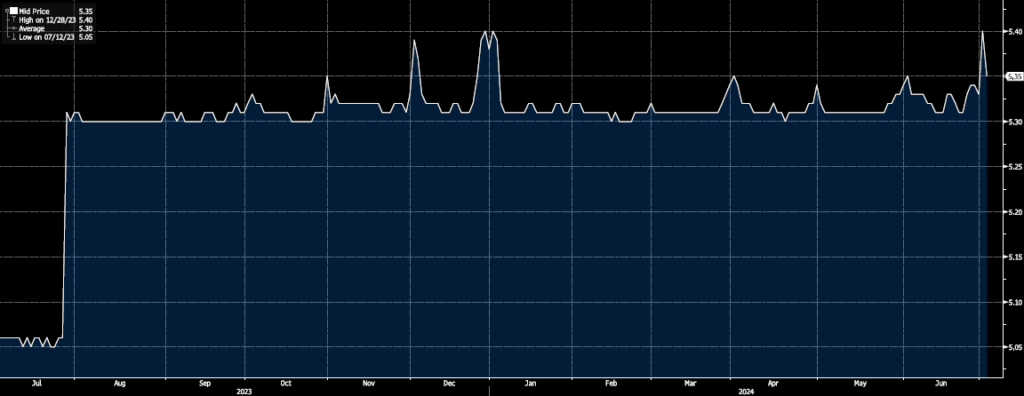

1. Secured Overnight Financing Rate* (Q2 2023 – Q2 2024)

We’ve been in a holding pattern with rates since the Fed’s last hike on July 27th, 2023 – almost a year ago. This is usually the pause before the storm leading up to a recession. Since the Fed has maintained a data driven decision making policy, they won’t take any action until the numbers say otherwise. But by the time the data is calling for a cut, it’s often already too late.

*SOFR is the average rate at which institutions can borrow US dollars overnight. It is currently the most common indices utilized to measure the short-term cost of borrowing for commercial real estate loans and will typically be used in conjunction with a bank spread to calculate a short-term, variable rate.

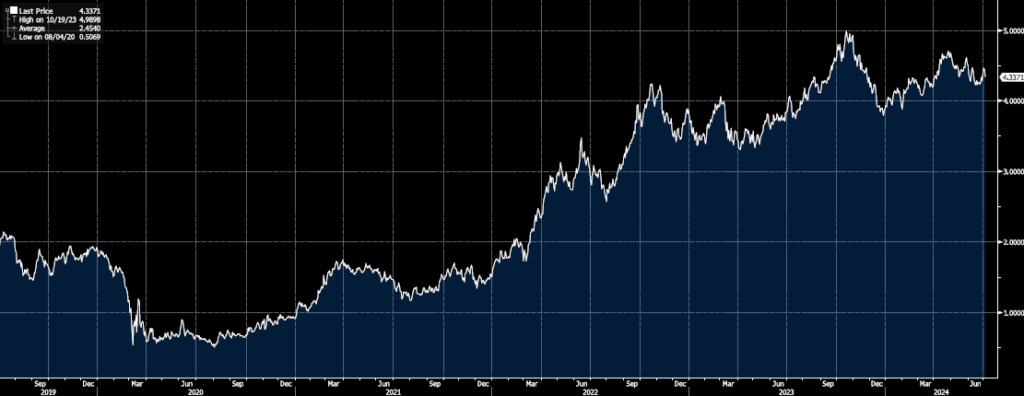

2. US 10-Year Treasury Yield* (Last 5 years)

The 10-year Treasury rate is currently hovering around 4.28%. Unlike short-term rates like the Fed Funds rate, the long end of the curve behaves differently. When the Fed makes its first cut to short-term rates, the 10-year rate is expected to drop quickly based on market expectations.

*The 10-year Treasury Yield is the return the government pays a purchaser for a 10-year treasury-backed bond. It is a good indicator of long-term interest rates and oftentimes close to the cost of a bank lending capital for an equivalent period.

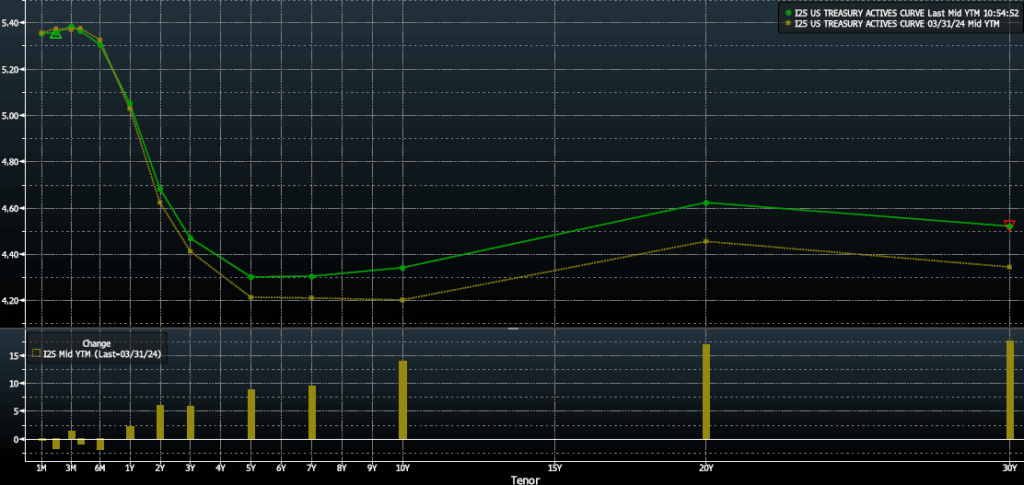

3. Treasury Yield Curve (Q2-2024 vs. Q1-2024)

We’re still in an inverted yield curve environment where the cost of long-term borrowing is cheaper than short-term borrowing. It can be noted that the interest rates across the curve are lower now than one quarter prior.

*Treasury yield curves demonstrate the relationship between interest rates and time to maturity. There are three main yield curve shapes: normal upward-sloping curve (where long-term rates are higher than short-term rates), inverted downward-sloping curve (where long-term rates are lower than short-term rates), and flat where interest rates are approximately the same regardless of tenor.

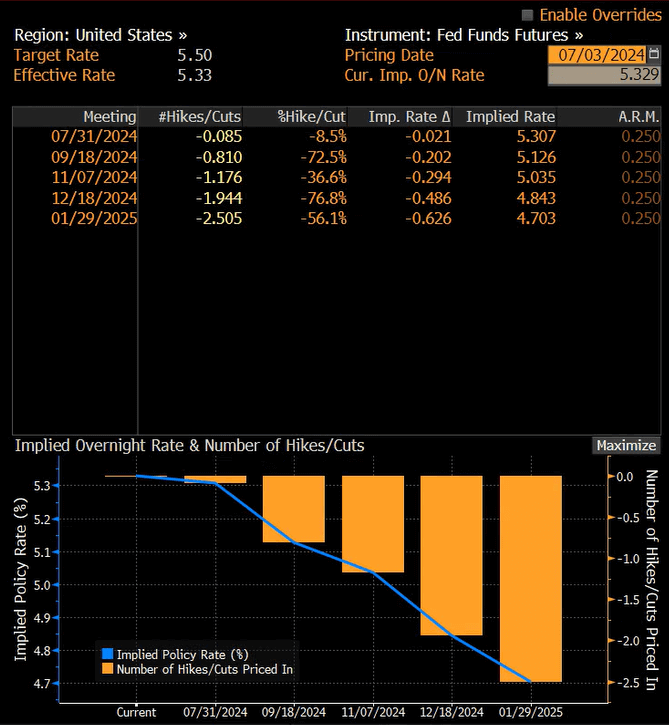

4. World Interest Rate Probability

The highest probability, just over 75% chance, of a rate cut based on market sentiment is at the September FOMC meeting this year. This feels a bit too close to the elections, but that’s never stopped the Fed before.

*Generally, if the market only prices in < 60% of a movement (hike or cut), there remains a lot of uncertainty as to what the Fed would do. When it approaches 60%, then it gets a little more serious. If the market is misaligned in that case, someone from the Fed will likely speak out to adjust market expectations.

by Chris Tollinchi

Share this ![]()