Share this ![]()

October 7, 2024

Football is back baby! My Bengals are Super Bowl-bound! … or, so I thought. After an 1-3 start, reality is sinking in. No worries though, my UCF Knights are charging on toward Big 12 dominance and a College Football Playoff appearance, am I right? Wait … never mind, we got stomped at home by Deion “Primetime” Sanders and Colorado. I guess it’s a good thing I’ve got a day job! At least Georgia’s reign ended (even if it was to Alabama). Misery loves company. Reality clearly differs from my expectations.

The silver lining is that the Fed came through with a 50-basis point rate cut at the September meeting – the first since 2020. For those of us living in the world of commercial real estate and debt financing, this was pure music to our ears. Does anyone else feel like they’re drinking from a fire hose right now? Activity has certainly picked up these past few weeks!

Economic Overview

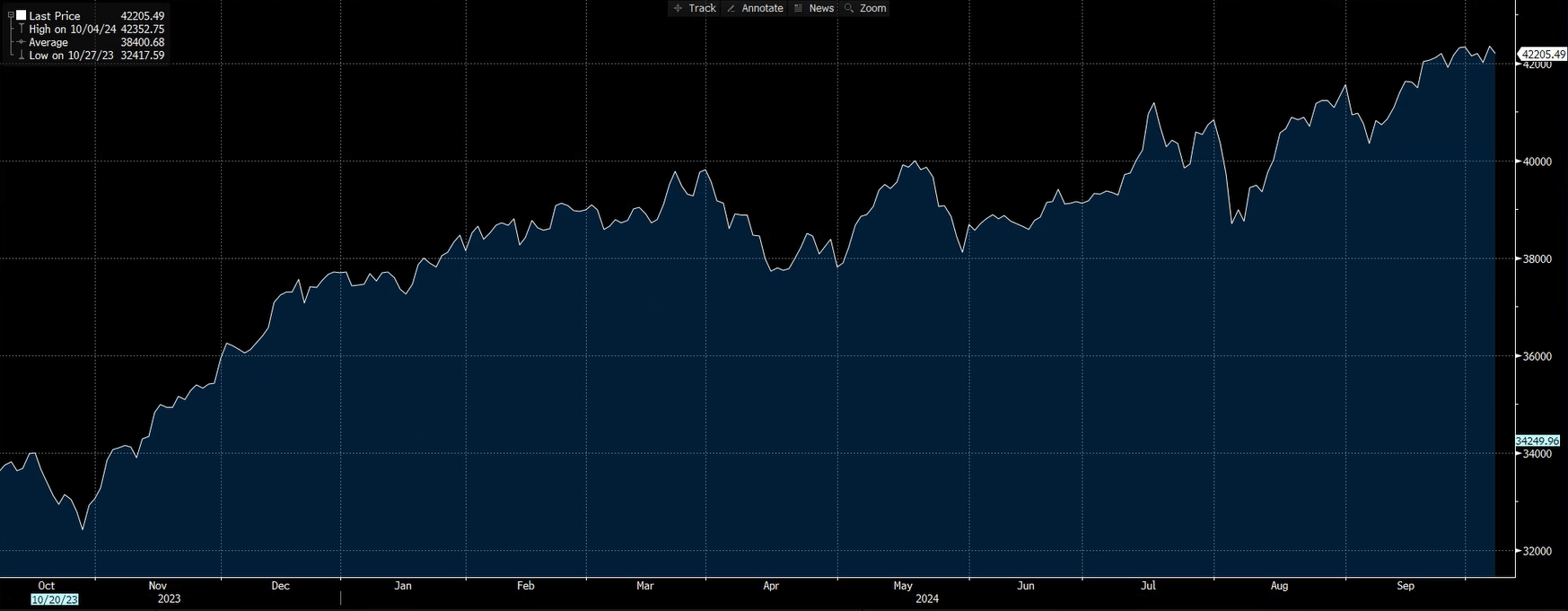

Inflation is finally slowing – currently down to 2.5% – though it seems to be at the cost of a softening job market, or one would think. Unemployment ticked up to 4.2%, which might have been an early indicator of more challenges ahead. But then it ticked back down to 4.1% in September. Mythical soft landing achieved? Mission accomplished for the Fed? Time will tell. But the latest jobs report virtually wipes out any chance for a double cut in November. As for equities, the rollercoaster ride continues, but there is a sense that the market is hanging on Jerome Powell’s every word.

Interest Rates: Short Term vs. Long Term

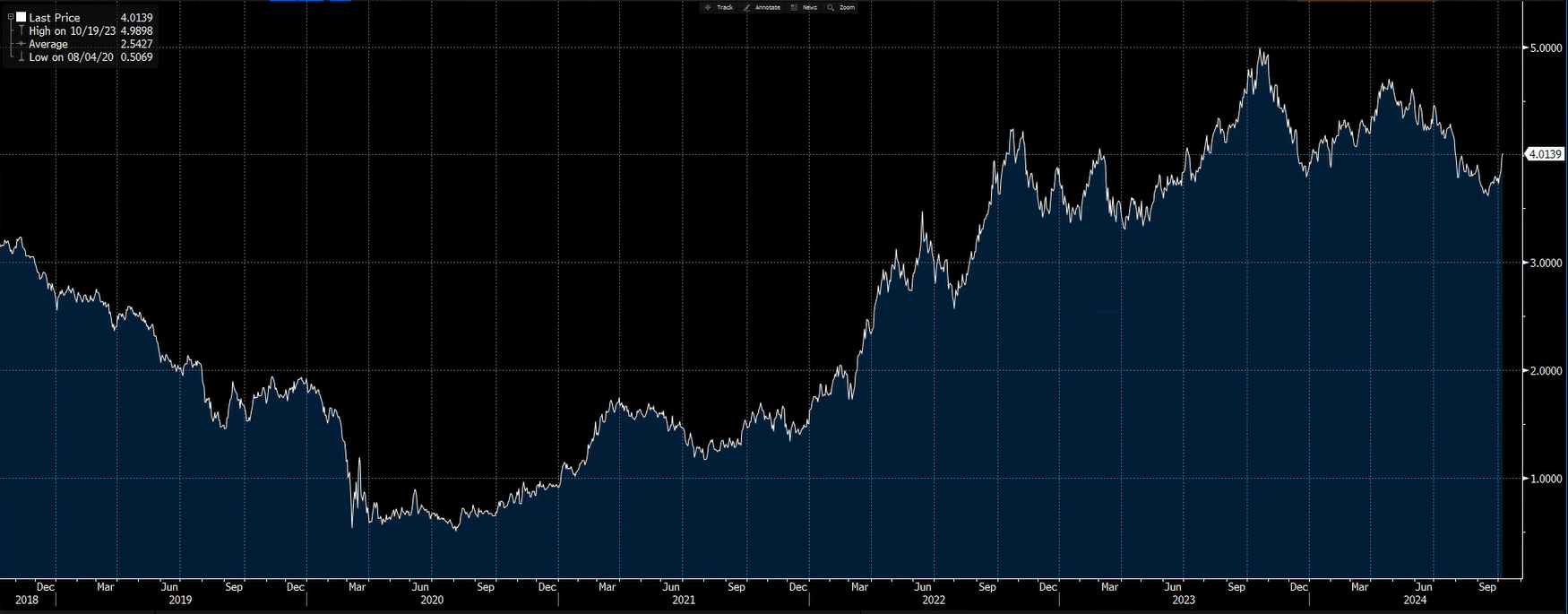

One of the common questions we’ve heard from borrowers lately is: Why aren’t long-term rates moving with short-term rates? When the Fed cuts 50-basis points, it’s easy to think all rates should follow suit. But the reality is short-term rates, like SOFR, are directly correlated and influenced by Fed policy. Long-term rates, however, move based on future market expectations.

So, when headlines announce a 50-basis point cut, borrowers naturally expect their 10-year loan rates to drop as well. After the cut was announced, however, long-term rates went up which is a signal the market over-estimated its expectation of future rates. The nuts and bolts of this is that bond prices and yields have an inverse relationship: when bond prices fall, yields (interest rates) go up. After the rate cut, bond traders started selling long-term bonds which caused bond prices to drop and long-term yields to rise. It’s a form of profit-taking or adjusting positions based on future expectations. Essentially, traders are unloading their bets to take profit which pushes long-term rates to go up.

Place Your Bets

For many of our borrowers, the current strategy has shifted towards shorter-term hedging to maintain flexibility. Let’s be clear though – long-term rates have fallen more than 100 basis points from their peak during this tightening cycle. So, the question remains: is there room for long-term rates to fall further? I think it’s fair to say that we won’t see COVID low again without a black swan event. The 10-year treasury trading around 3.50% feels reasonable and still aligns with the Fed’s “higher for longer” mantra.

In football, you gameplan as best you can, adjusting as you go. Games are won in the fourth quarter. The same could be said in business – whether it’s closing deals or navigating rate fluctuations, success in the fourth quarter comes down to strategy, flexibility, and sometimes, just grit and the will to get the job done. Let’s finish strong! #whodey #GKCO

by Chris Tollinchi

Share this ![]()