Share this ![]()

July 27, 2025

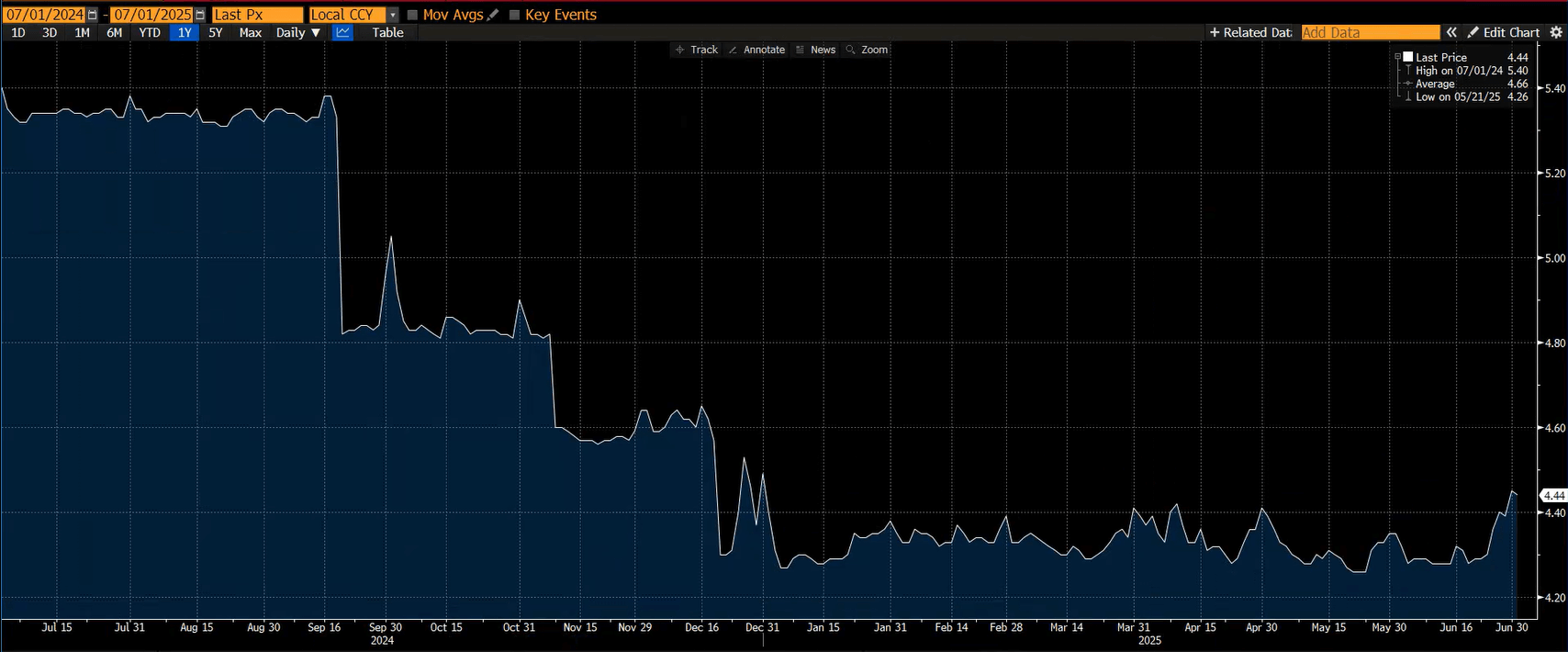

1. Secured Overnight Financing Rate* (Q2 2024 – Q2 2025)

SOFR remains steady at around 4.30-4.45% until the Fed takes further action.

*SOFR is the average rate at which institutions can borrow US dollars overnight. It is currently the most common indices utilized to measure the short-term cost of borrowing for commercial real estate loans and will typically be used in conjunction with a bank spread to calculate a short-term, variable rate.

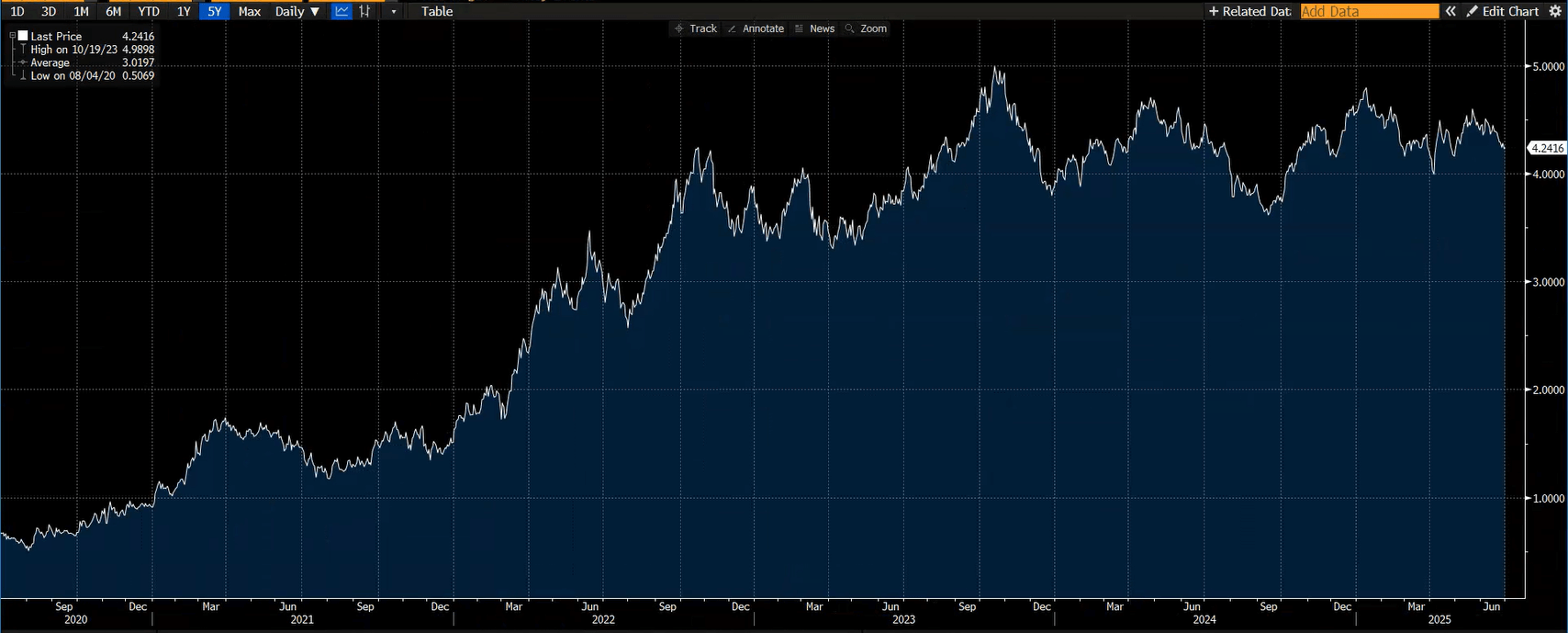

2. US 10-Year Treasury yield* (Last 5 years)

Over the past quarter, even with tariff-induced volatility, the 10-year Treasury rate has remained stable, averaging around 4.3%. This indicates market indecision and cautious optimism as investors gauge the likelihood of future rate cuts.

*The 10-year Treasury Yield is the return the government pays a purchaser for a 10-year treasury-backed bond. It is a good indicator of long-term interest rates and is oftentimes close to the cost of a bank lending capital for an equivalent period.

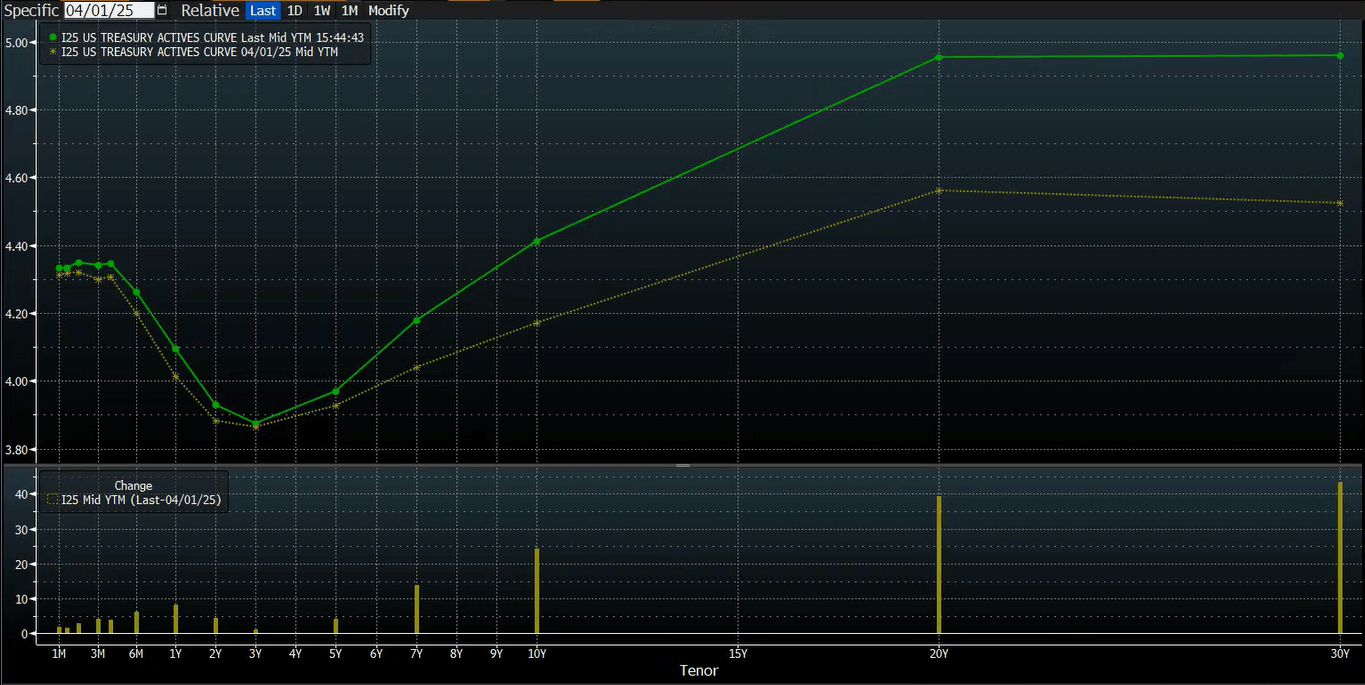

3. Treasury Yield Curve (Q2-2025 vs. Q1-2025)

Longer-tenor rates have increased over the past quarter, steepening the yield curve.

*Treasury yield curves demonstrate the relationship between interest rates and time to maturity. There are three main yield curve shapes: normal upward-sloping curve (where long-term rates are higher than short-term rates), inverted downward-sloping curve (where long-term rates are lower than short-term rates), and flat where interest rates are approximately the same regardless of tenor.

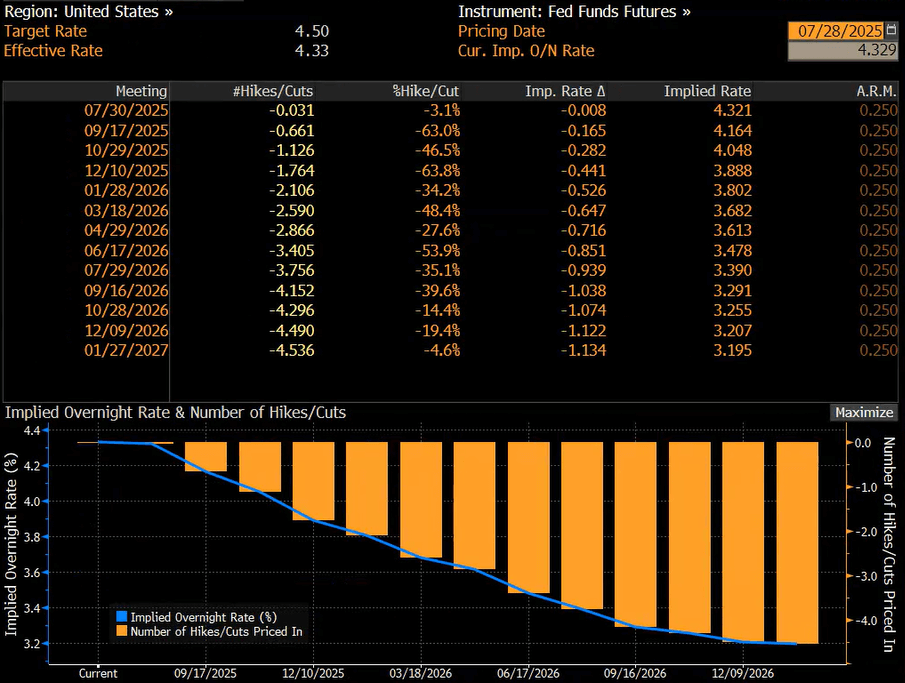

4. World Interest Rate Probability

The market is assigning ~66% probability of a rate cut at the September FOMC meeting.

by - CMAC

Share this ![]()