Share this ![]()

July 27, 2025

This summer has been one of those fleeting, golden windows in life—equal parts exhausting and magical. I’ve spent it with my two kids (ages 3 and 5), and I think we’ve officially entered what might be the “golden age” of parenting. Both kids can dress themselves, both are more or less potty-trained, and we’re finally having conversations that almost resemble logic (life is good!). That said, I still find myself playing hostage negotiator at the dinner table—my daughter (the 3-year-old) is very particular about who she sits next to.

Some nights, I walk away from the dinner table feeling like I’ve taken crazy pills—any parent who’s been through this stage knows exactly what I mean. But in all seriousness, the summer has flown by, and now we’re staring down kindergarten next month. I’m still trying to wrap my head around that one.

All this reflection has me thinking about the broader economy. It feels like we just managed to get a handle on inflation (maybe), wrapped up the emergency policy playbook from the COVID era… and now we’re already talking about cutting rates and possibly replacing Fed Chair Jerome Powell? It’s hard to keep up.

Forgive the crassness, but… what?!

I’m no PhD economist, but my basic understanding of policy is pretty straightforward: if the economy is doing well, you generally hold rates steady —or even raise them—depending on just how well things are going. That’s just sound macroeconomic principle.

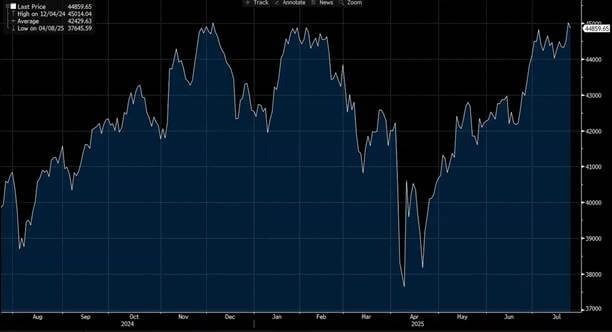

(Dow Jones Industrial Average)

Adding Fuel to the Fire

And now, we’re throwing tariffs into the mix. Countries like Japan, China, and the UK have already struck agreements with the U.S., while others—like Canada, the EU, and Mexico—remain in negotiation. Over time, these tariffs might benefit U.S. manufacturing and reduce trade deficits. But make no mistake: in the short term, they can be inflationary.

As a commercial real estate loan consultant, I’ll admit—rate cuts are usually music to my ears. But at what cost? Right now, it feels premature. Too much like a short-term play that risks fueling asset bubbles, reigniting inflation, and ultimately leading to a correction.

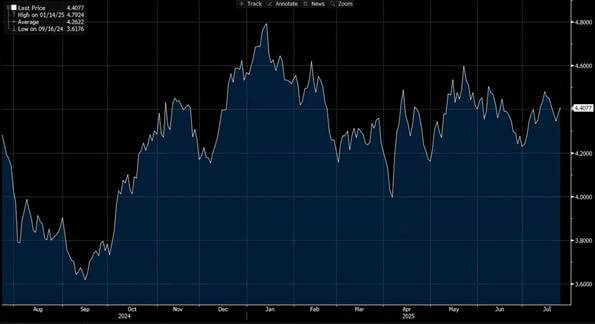

(10-Year Treasury Rates)

The Foggy Crystal Ball

Look, I’m 50/50 on this—maybe even 49/51. I could be wrong. Maybe this is all part of a finely tuned plan and everything’s under control. But from where I sit, it feels more like a setup for déjà vu than a sustainable strategy.

We’ve seen this before:

Cut rates into strength.

Chase growth.

Inflate valuations.

And then eventually… the bill comes due.

(There’s a pattern here.)

Dot-com bubble.

Housing bubble.

Post-COVID stimulus wave.

We know how this movie ends.

Roll Credits

There’s a saying in finance: “Don’t fight the Fed.” But my gut tells me the White House might win this round. Then again—what do I know? I’m just a dad with a keyboard, trying to close loans and keep my kids from fighting each other. That said, I’m seeing it firsthand: more clients are choosing to float their rates, leaning into the promise of future cuts rather than locking in today’s certainty.

by Chris Tollinchi

Share this ![]()