Share this ![]()

October 13, 2025

If summer was the “golden age” of parenting, fall has ushered in what I can only describe as the “threenager era.” My daughter has suddenly developed strong opinions on everything from which socks she’ll wear to who’s allowed to pour her milk. She’s fierce, funny, and fully committed to chaos.

She’s a perfect reflection of the market right now.

One minute she’s thrilled, laughing, dancing around the living room, and the next she’s melting down because her banana broke in half. That’s the energy we’ve been living in, both at home and in the marketplace.

Like a toddler’s emotional range, the shifts are coming fast and without warning. We’ve gone from confidently pricing in a soft landing to now expecting two (possibly three) more rate cuts by the end of the year.

Between double-cut chatter and the government shutdown, the markets are basically living the same emotional rollercoaster as my three-year-old. Calm one minute, crisis the next.

(What’s that over there? Oh, right, those tariffs we talked about last quarter.)

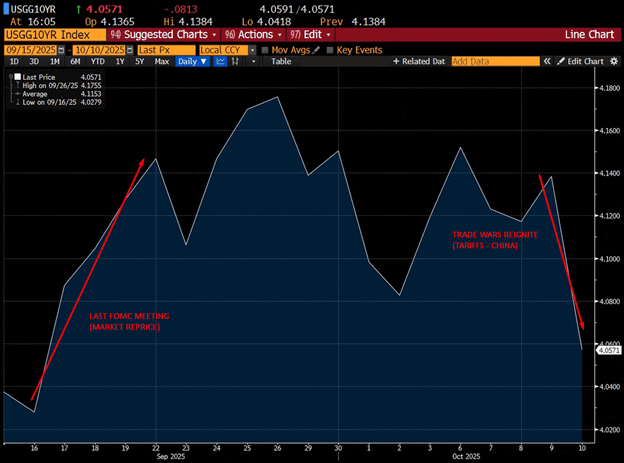

The markets are reacting exactly how you might expect: yields have slipped almost 10 basis points on 10-year money as investors recalibrate for the inflationary drag tariffs bring. The irony, of course, is that tariffs are supposed to strengthen domestic production. But in practice, they ripple through the system like a toddler’s mood: messy, unpredictable, and not always rational.

(10-year treasury rate from September 15th 2025 to October 10th 2025)

Fool Me Once, Shame on You. Fool Me Twice…

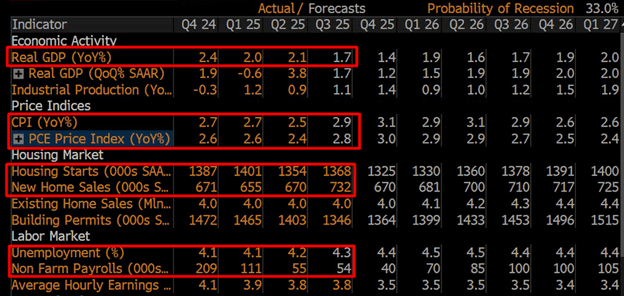

If the current projections hold, we’re headed for back-to-back cuts before year-end. That’s a lot of optimism baked into the cake, especially given that the economy (at least on the surface) still looks “resilient.” GDP is down. Headline CPI has ticked up from 2.5% to 2.9%; quarter over quarter. Core CPI remains sticky at 3.0%. Housing sales have ticked up while unemployment remains low. Credit markets haven’t seized. We’re actually seeing the most aggressive pricing we’ve seen in years, and borrowers remain active.

(Economic Forecast quarterly view for 2024-2025 with projections beyond)

So, while the administration may point the finger at Powell for moving too slowly, the Fed Chair might just be the parent in the room, trying to keep the economy from throwing a total tantrum in public.

Where We Go From Here

As for what’s next? Your guess is as good as mine. My read is that we’re entering a stretch of emotional volatility: some sugar-induced highs, a few time-outs, and the occasional breakthrough moments of calm. Opportunities will exist. Borrowers who can stay patient and flexible will find them in the noise.

Like life with a three-year-old, it’ll look peaceful for all of five minutes…right before someone dumps a gallon of apple juice on the floor and laughs.

by Chris Tollinchi

Share this ![]()