Share this ![]()

October 13, 2025

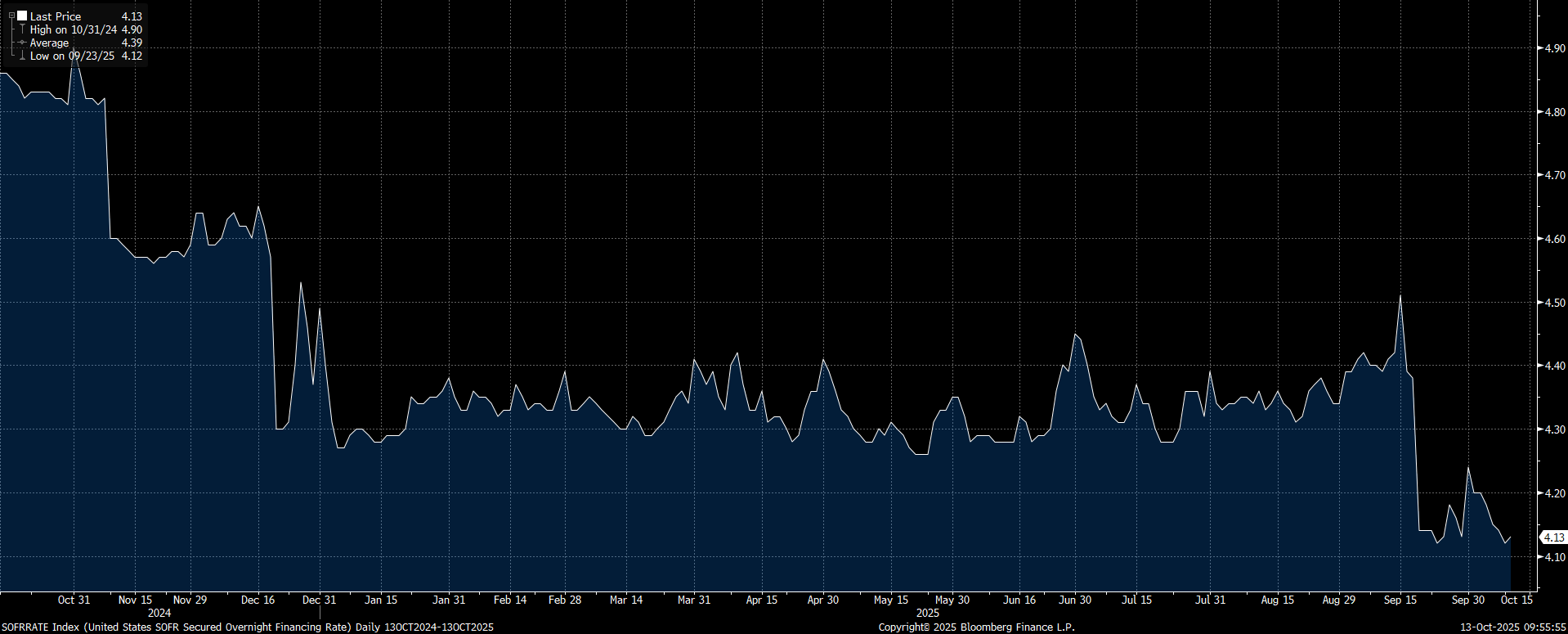

1. Secured Overnight Financing Rate* (Q3 2024 – Q3 2025)

SOFR remains range-bound with a target rate of 4.25% until the Fed meets at the end of the month on October 29th, 2025.

*SOFR is the average rate at which institutions can borrow US dollars overnight. It is currently the most common indices utilized to measure the short-term cost of borrowing for commercial real estate loans and will typically be used in conjunction with a bank spread to calculate a short-term, variable rate.

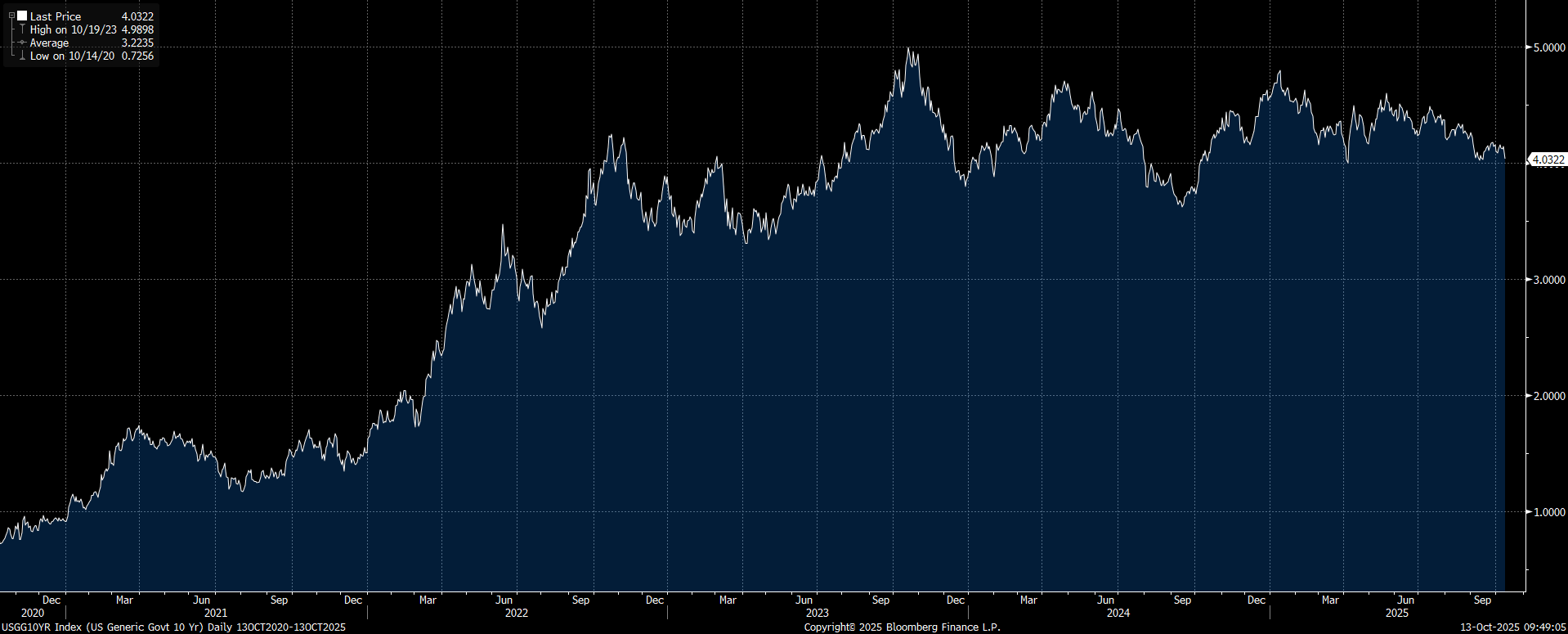

2. US 10-Year Treasury yield* (Last 5 years)

Over the past 3–6 months, the 10-year U.S. Treasury yield has generally trended upward, fluctuating between 4.2% and 4.6% as markets weighed inflation data and shifting Fed expectations. After climbing through early fall on stronger economic readings, yields eased back to around 4.4% as of Friday, reflecting renewed optimism about potential rate cuts in 2026. The recent pullback suggests investors are reassessing the pace of cooling inflation.

*The 10-year Treasury Yield is the return the government pays a purchaser for a 10-year treasury-backed bond. It is a good indicator of long-term interest rates and is oftentimes close to the cost of a bank lending capital for an equivalent period.

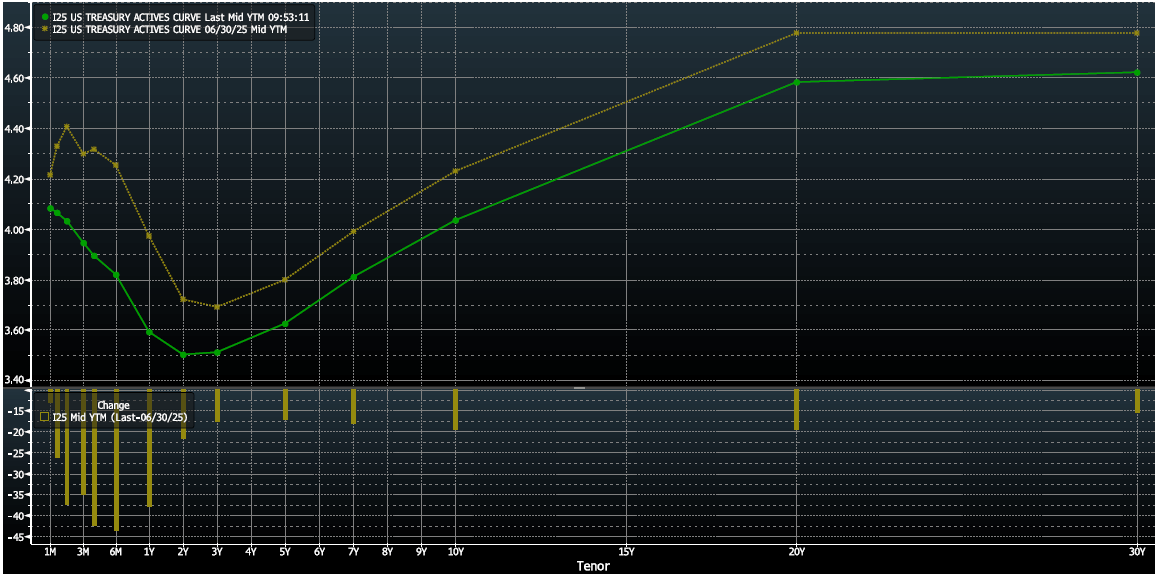

3. Treasury Yield Curve* (Q2-2025 vs. Q3-2025)

U.S. Treasury yield curve has been flattened to modestly inverted in key segments: short-term rates (e.g. 2- and 3-month) have occasionally exceeded longer maturities. The 10-year minus 2-year spread is still positive (about 0.53% as of October), but the 10-year minus 3-month spread is nearly flat (around 0.03%), highlighting pronounced tension between the short and long ends of the curve.

*Treasury yield curves demonstrate the relationship between interest rates and time to maturity. There are three main yield curve shapes: normal upward-sloping curve (where long-term rates are higher than short-term rates), inverted downward-sloping curve (where long-term rates are lower than short-term rates), and flat where interest rates are approximately the same regardless of tenor.

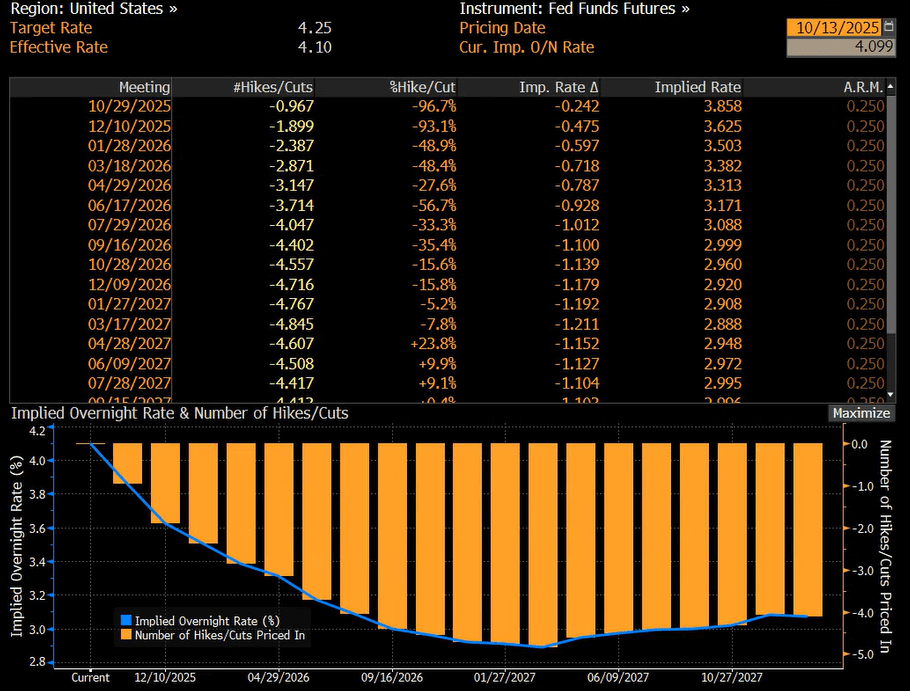

4. World Interest Rate Probability

Markets are currently pricing in near-certainty of at least a 25-basis-point rate cut at each of the next two Federal Reserve meetings to close out the year. There also remains a modest probability of larger 50-basis-point cuts being priced in at both meetings, with markets likely to make rapid adjustments before and after each announcement as incoming data and Fed commentary shape expectations.

The WIRP function on Bloomberg, short for “World Interest Rate Probability”, is a tool that shows market-implied probabilities of central bank rate changes for upcoming policy meetings. It derives these probabilities from futures and OIS (overnight index swap) pricing, translating where markets are trading into the implied odds of rate hikes, cuts, or holds at specific meeting dates.

by - CMAC

Share this ![]()