Share this ![]()

May 25, 2022

At the request of the Congress of Physician-Owned Medical Properties (CPOMP), CMAC Partners has released 5 of its proprietary models that have been developed and refined over the last 15 years. They are being shared to continue CMAC’s mission of making physician groups stronger through their medical real estate investment. The models provide a comprehensive range of analyses on real estate structuring and measuring investment performance. Here is a look at how the top 5 might assist your group:

TruCourse 2.0: Succession Management Tool

Allows you to model your entity’s buy-in and buyout structure over a 15-year period. Probability-based forecasting allows groups to optimize variables in their operating agreement in order to improve succession planning outcomes. Ideal for groups in the process of addressing concerns during the creation of their operating agreement or revamping an existing operating agreement.

Physician Owner Re-syndication Model

Enables a real estate entity to create an attractive investment for a new owner while assuring retiring partners of full buyout value. The re-syndication model offers a methodology for affordably diluting existing owners and realigning the interest of the real estate to the ownership of the practice.

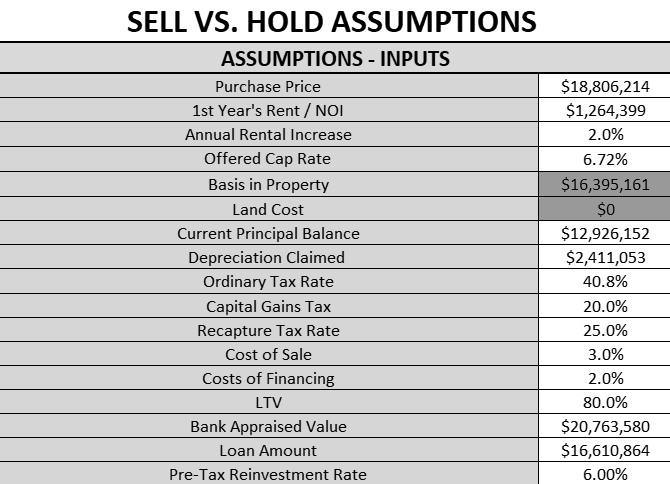

Economic Outcomes and Equity Gain Model

Provides insight into the economic effects of differing levels of ownership in your real estate project. Most importantly, it demonstrates the inequities associated with giving up large portions of the ownership to outside partners and the impact minority ownership has on a project’s IRR. It quantifies options so that partners can make informed decisions

New Partner Equity Breakeven Model

This model applies a set of macros to the stream of cash flows produced by the real estate investment, net of taxes, to calculate how much can be borrowed personally while remaining cash flow neutral. Oftentimes, this reduces the cash required for equity by greater than 75% and the new physicians do not have to come out of pocket again. Most banks are open and willing to make such loans when negotiated alongside the entity debt.

Loan Savings Analysis

This model takes any number of bank proposals and quantifies the differences in interest rates, amortizations, loan origination fees and debt service coverage ratios to provide both resultant net interest costs and cash flow differentials. Available with both a simple and complex version.

To find out more about these models and how they can be customized to meet your needs email solutions@cmacpartners.com.

by - CMAC

Share this ![]()