Share this ![]()

October 7, 2024

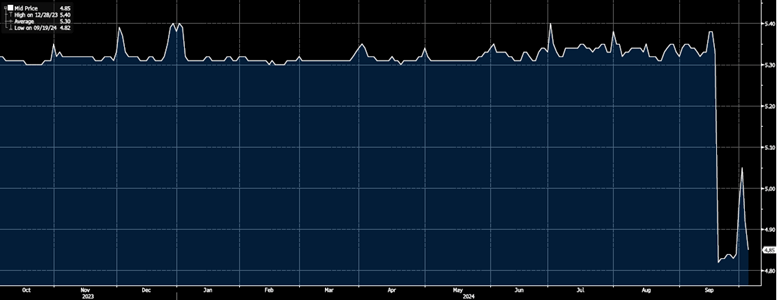

1. Secured Overnight Financing Rate* (Q3 2023 – Q3 2024)

The Federal Reserve’s recent decision to cut interest rates by 50 basis points signals a shift in monetary policy aimed at stabilizing economic growth amid cooling inflation. As seen with short-term rate indices like SOFR, these rates react immediately in direct correlation with changes to the Fed Funds rate. This move will lower borrowing costs for borrowers with floating-rate loans who are not otherwise hedged against volatility

*SOFR is the average rate at which institutions can borrow US dollars overnight. It is currently the most common indices utilized to measure the short-term cost of borrowing for commercial real estate loans and will typically be used in conjunction with a bank spread to calculate a short-term, variable rate.

2. US 10-Year Treasury yield* (Last 5 years)

The recent decline in 10-year Treasury rates, dropping from a peak of 4.70% in late April to the current low of 3.96%, reflects a shift in market sentiment amid growing concerns over slower economic growth and easing inflation pressures. As the graph illustrates, this downward trend in long-term yields suggests a more cautious outlook from investors, which could result in more favorable borrowing costs for long-term fixed-rate loans.

*The 10-year Treasury Yield is the return the government pays a purchaser for a 10-year treasury backed bond. It is a good indicator of long-term interest rates and oftentimes close to the cost of a bank lending capital for an equivalent period.

3. Treasury Yield Curve (Q3-2024 vs. Q2-2024)

The current Treasury yield curve is flattening, particularly between the 2-year (3.93%) and 10-year (3.97%) maturities. This flattening is typical toward the end of a monetary tightening cycle, where short-term rates remain elevated due to past rate hikes, while long-term rates reflect growing expectations of an economic slowdown or potential future rate cuts.

*Treasury yield curves demonstrate the relationship between interest rates and time to maturity. There are three main yield curve shapes: normal upward-sloping curve (where long-term rates are higher than short-term rates), inverted downward-sloping curve (where long-term rates are lower than short-term rates), and flat where interest rates are approximately the same regardless of tenor.

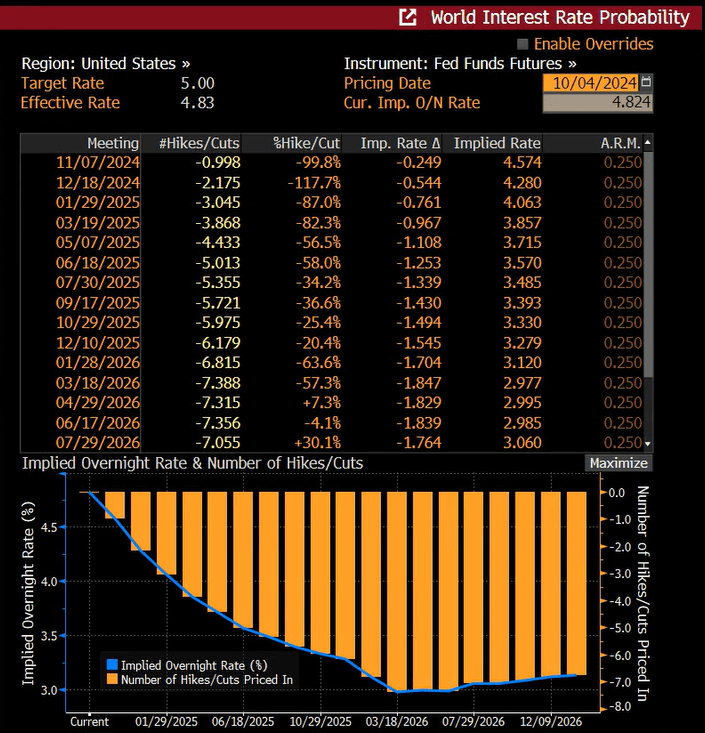

4. World Interest Rate Probability

Prior to today’s jobs report, market pricing reflected a 30% to 40% probability of a double rate cut at the November FOMC meeting. However, following the report's release, the probability has shifted, with markets now fully pricing in a single 25-basis point rate cut next month, and the chance of a double rate cut in December dropping to just 17%.

by Ha Tran - Finance Project Manager

Share this ![]()