Share this ![]()

January 13, 2025

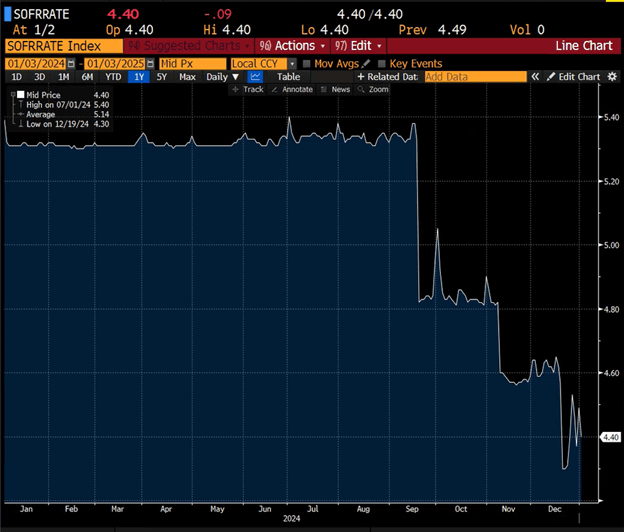

1. Secured Overnight Financing Rate* (Q4 2023 – Q4 2024)

At the end of Q3 the Federal Reserve decided to cut interest rates by 50 basis points, and followed this up with an additional two 25 basis point cuts in Q4, trimming the Fed Funds rate and short-term rate indices like SOFR by 1% in total since the beginning of the year. This move will lower borrowing costs for borrowers with floating-rate loans.

*SOFR is the average rate at which institutions can borrow US dollars overnight. It is currently the most common indices utilized to measure the short-term cost of borrowing for commercial real estate loans and will typically be used in conjunction with a bank spread to calculate a short-term, variable rate.

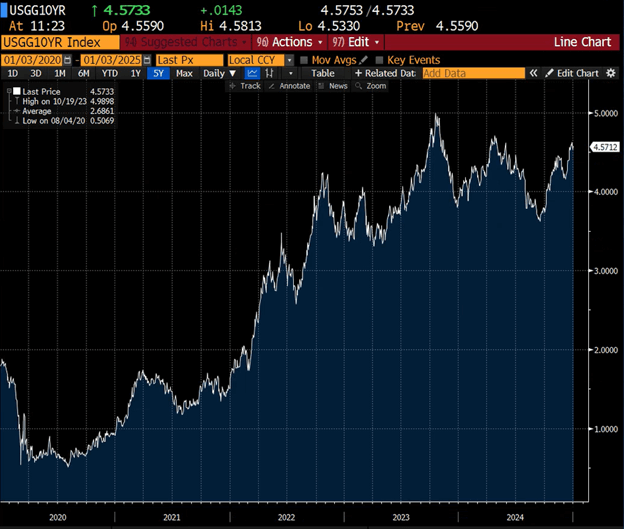

2. US 10-Year Treasury yield* (Last 5 years)

The 10-year Treasury rate bumped back up in Q4, rising 77 basis points from 3.81% at the end of Q3 to 4.58% at the end of Q4. The initial surge was driven by the US Presidential election, as investors bet a Trump presidency would increase economic growth and fiscal spending. The continued increase has been propelled by a shift in expectations of future rate cuts. Growing concerns over sticky inflation mixed with Powell’s recent messaging has lowered expectations for future rate cuts, resulting in higher long-term rate expectations. This change will result in less favorable borrowing costs for long-term fixed-rate loans.

*The 10-year Treasury Yield is the return the government pays a purchaser for a 10-year treasury-backed bond. It is a good indicator of long-term interest rates and is oftentimes close to the cost of a bank lending capital for an equivalent period.

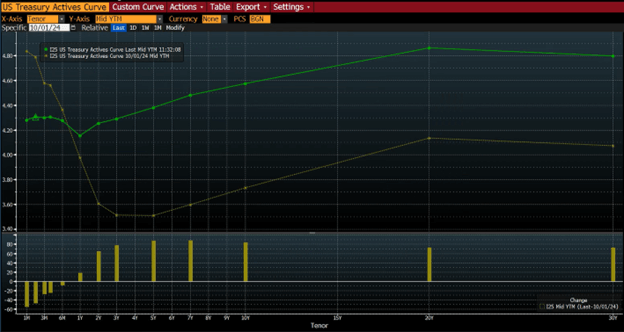

3. Treasury Yield Curve (Q4-2024 vs. Q3-2024)

The 2Y treasury closed the year at 4.25%, while the 10Y treasury closed the year at 4.58%. This tells us that the cost of borrowing for shorter-term loans is beginning to cost less again than the cost of long-term loans. In the past quarter, we’ve also seen an increase in the cost of borrowing across the majority of the curve.

*Treasury yield curves demonstrate the relationship between interest rates and time to maturity. There are three main yield curve shapes: normal upward-sloping curve (where long-term rates are higher than short-term rates), inverted downward-sloping curve (where long-term rates are lower than short-term rates), and flat where interest rates are approximately the same regardless of tenor.

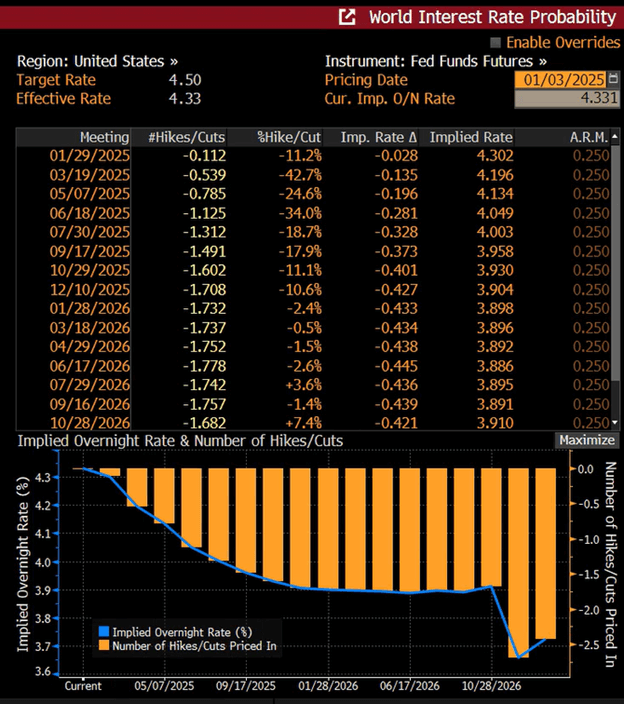

4. World Interest Rate Probability

The general consensus is that the Fed will pause during the January meeting, with the market predicting an 11% probability of a cut. Market data including the job and inflation reports will largely dictate the number of cuts in 2025, with the market now projecting just 2 cuts in total.

by Grant Blackhurst - Senior Analyst

Share this ![]()