Share this ![]()

January 23, 2026

Level the playing field with a swap advisor to ensure you don’t lose when executing an interest rate swap

Did you use an interest rate swap to lock your interest rate? If so, do you have any idea what your swap spread was at the time of execution? Chances are … probably not.

The reason I can say this with confidence is because the swap spread - the profit taken by the swap desk - is never transparent. Many borrowers don’t recognize that the swap desk operates independently from your banking relationship manager. More importantly, the swap desk isn’t required to disclose this spread (the profit they make). That’s why you won’t find it in any of your loan or swap documents. This information asymmetry puts the bank firmly in the driver’s seat - while your group is taken for a ride.

Taking a quick step back - an interest rate swap is a method commonly used by lenders to synthetically fix your interest rate. It can be a valuable resource that allows groups to improve their interest rate. Essentially, it’s a separate contract layered on top of your loan to exchange a variable interest rate for a fixed interest rate.

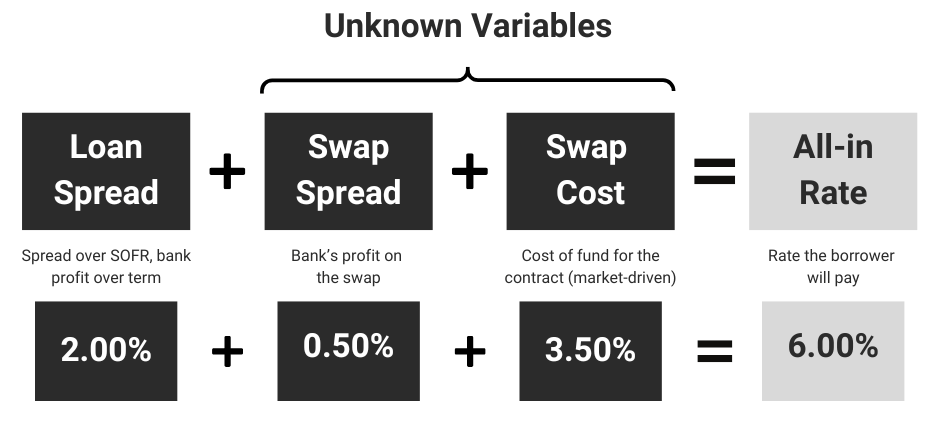

When reviewing your bank’s proposal and, later, the loan documents, the loan spread - the bank’s profit from the loan - is usually easy to spot. For instance, the bank may state your interest rate as Term SOFR (the floating rate index) + 2.00%, meaning their profit margin on the loan is 2%. If you choose not to enter an interest rate swap, your loan would float based on this index plus a 2% spread.

Sometimes, if you ask the right questions (or get lucky), the bank may state what the indicative interest rate would be on your proposal if you were to fix the rate with a swap. But what’s never disclosed - neither in the proposal nor in the final documents - is the swap spread (the profit the swap desk takes when fixing your rate).

Unless you have access to live market data - such as a Bloomberg terminal that allows you to price up the cost for a specific swap structure on a given time and day - you won’t have the ability to determine this key piece of information.

Using the same example, let’s say the bank quotes an indicative fixed rate of 6.00%. To uncover the hidden swap spread, you’d need to determine the cost of funds for the given swap structure - on the same day and at the same time the bank proposed. Suppose the cost of funds was 3.50% and, as mentioned above, the loan spread was 2%. That would imply a 50 basis point (bps) swap spread.

A 50 bps swap spread would be considered an excessive level of profit for a swap desk to take on a transaction - yet it’s often hidden from borrowers throughout the entire process. What’s more, this swap spread is arguably more impactful than the loan spread. That’s because the swap desk recognizes this profit immediately, on the day the swap is executed.

Here’s how it works: the swap desk takes the 0.50% interest per annum, multiplies it over the life of the swap, and present values it back to day 1 to capture it as an upfront fee. On a $20 million swap with a 10-year term and 25-year amortization, that could amount to approximately $759,000 in profit at execution (present value of each 0.01% = ~$15,180 x 50).

The swap spread becomes an embedded prepayment penalty that’s carried forward. The swap desk will either receive this profit over time as you pay the interest rate or, if you terminate the swap early, it will be factored into the swap unwind calculation. Either way, this ~$759k is a sunk cost that the borrower cannot recover.

Even if you’ve clarified the swap spread with your lender during negotiations, there’s nothing stopping the swap desk from taking additional swap profit at execution - unless you have access to live market data to verify the swap spread they’re taking on the stated fixed rate. We’ve been on swap execution calls with clients where the swap desk attempted to slip in an extra 10 bps above the agreed-upon swap spread. In the prior example, that would have quietly added $150,000 in hidden costs to the borrower - had it not been caught. I hesitate to imagine what they might have added if a swap advisor wasn’t present to hold them accountable.

So, how does having a swap advisor help alleviate this problem?

1. Pricing Transparency to Uncover Hidden Costs

A swap advisor with access to live market data, the right tools, and expertise can accurately price up the cost of funds for your given swap structure. This enables you to isolate the swap spread and ensure it’s adhered to on the day of execution, removing the information asymmetry from the process.

2. Market Knowledge to Strengthen Negotiations

It’s reasonable for a lender to charge a swap spread - but how much is too much? A seasoned swap advisor can benchmark your transaction against similar deals, provide a sense of what’s fair, and help negotiate a more competitive spread for your group.

3. Expertise to Align Swap Structure with Specific Goals

Interest rate swaps are highly customizable products. There are various hedging strategies that can be adopted to match your group’s objectives and philosophies.

- Have a greater risk tolerance, or confident that short-term rates will fall? You might want to fix a portion of the debt and leave some floating to take advantage of a potentially lower rate.

- Expecting to refinance before the term of the loan? You might consider swapping for a shorter term.

An advisor can help you navigate the different options and find one best suited for your needs.

To put it in perspective: if you were involved in a multi-million dollar lawsuit, would you represent yourself in court? You can execute a swap on your own - but that doesn’t mean you should. Regardless of whether or not you choose to use CMAC Partners, we strongly recommend working with an experienced swap expert to avoid unnecessary, hidden costs and ensure your structure is aligned with your best interests.

by Grant Blackhurst - Senior Analyst

Share this ![]()