Share this ![]()

October 20, 2023

Like when teenagers stopped wearing Crocs in the late 2000s (thanks, Justin Bieber, for bringing back that trend), change is sometimes for the better. Another example of this has occurred in recent years: a consistent and justifiable movement away from using appraisals to value partner buy-ins and buyouts of real estate entities. Unlike Crocs, the primary reason for the “appraisal boycott” trend is inconsistency (because Crocs are consistently bad, obviously).

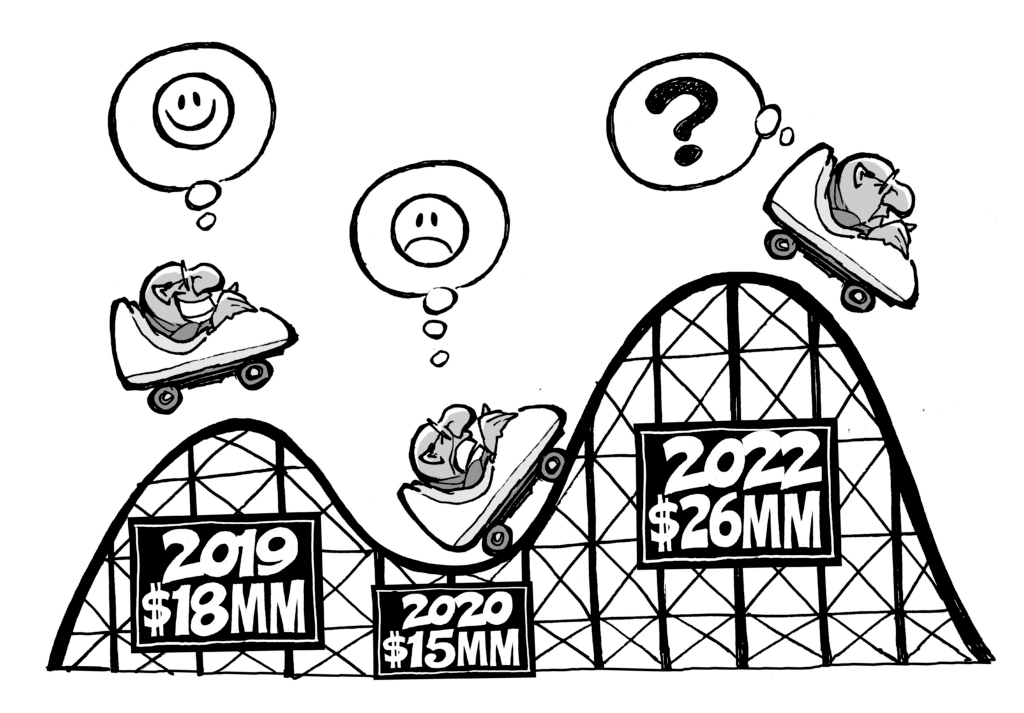

Appraisals are, by definition, a single individual’s opinion of value. Yes, there are some numbers (comps) that are used to support the claim, but we have seen deviations of >25% caused merely by which comps are picked (or disregarded). Take the example of Midwest Orthopedics. Their real estate went from an $18MM valuation in 2019 to a $15MM valuation in 2020 before finally receiving an appraised value at $26MM in 2022. With the debt included, each partner in the group went from $300,000 of equity in 2019 to $0 in 2020 to $800,000 in 2022. The only thing that changed was the appraiser’s opinion of value.

But that begs a bigger question. What cheap and consistent valuation methodologies would allow us to achieve a sustainable partner succession plan without creating inequities? Let’s explore the primary alternative.

Income Capitalization: The Leading Alternative

Since commercial properties are income producing, their value is ultimately derived from the amount, consistency, and longevity of the income produced. Therefore, a vast majority of the building’s value can be found in the lease agreement. That said, it is possible to create a consistent and reliable valuation by applying a multiple of the base rent. Let’s explore an example: Say a building is producing $1MM of annual rental income. If you apply a multiple of 12.5x, you end up with a building valuation of 12.5MM. For those readers familiar with cap rates, that is the same as applying an 8% capitalization rate to the building ($1MM divided by 8% = $12.5MM).

This methodology is particularly enticing for a couple of reasons. First, it utilizes the same mechanism that third parties adopt when acquiring a medical office building in a sale/leaseback transaction, which allows for market-driven examples of how outside parties value the income the building creates. Second, and perhaps most impactful, it creates predictable, stable buyout values and consistent returns. Because the real estate valuation is directly proportional to the lease income, as the leases escalate, so does the value of the building, therefore, maintaining the same return on investment.

Now for the tricky part. What capitalization rate makes sense for a specific building or set of buildings? In our experience, there are no hard and fast rules surrounding the exact number; however, there are a few variables that should be considered before deciding on an outcome.

Generally, the easiest place to start is by understanding the value at which a third party would be willing to purchase the building under a long-term lease arrangement (between 10-12 years). Let’s say that the buyer asks for a 6% capitalization rate, meaning the purchase price equals the annual rental income divided by 6%. With that in mind, there are two factors one should consider when determining a number relative to a third-party calculation.

- You are assessing the value of an individual’s share and not that of an entity. Because no single individual has controlling rights, there is typically a discount applied for the lack of marketability associated with that non-controlling interest.

- The third-party sale valuation described above takes into consideration that the practice will maintain a long-term obligation that is driving the value – an obligation that a partner being bought out is not contributing to. Therefore, it would be nonsensical to buy out a partner based on a valuation that the partner has not contributed to creating.

With these two points in mind, we typically see that a discount is applied relative to a third-party market valuation of anywhere between 1% - 3% (in cap rate terms). This means that the ascribed building valuation in the example above would result in a valuation of anywhere between a 7% - 9% cap rate ($14.29MM - $11.11MM).

So, now that you have a valuation methodology that is measurable and consistent, we advise that you put together a long-term model to test, report, and manage the investment. Mentes360, an interactive program created by CMAC Partners, does just that. Based on your group’s demographics and defined structure, Mentes360 creates a model that allows you to understand the following variables:

- The impact of different capitalization rates

- The expected return for each partner (inclusive of buyout)

- The effect of buy-ins and buyout notes

- The impact of completing periodic cash-out refinances vs. paying down the debt

- The implications of a minimum investment horizon

For more information, reach out to support@mentes360.com.

by Ha Tran - Finance Project Manager

Share this ![]()